Strong Margins, High Cash Flow, Deposit Open

Stornoway Diamond Corporation (TSX-SWY) is pleased to announce the results of the Feasibility Study (“FS”) for the Renard Diamond Project located in North Central Québec. The FS outlines a combined open pit and underground mine plan and was prepared by SNC Lavalin Inc. with contributions from AMEC Americas Ltd (“AMEC”) for the design of the underground mine and diamond processing plant and G Mining Services Inc. (“G Mining”) for open pit mine design and cash flow analysis. Additional technical elements of the study have been authored by Roche Ltd., Golder Associates Ltd. and Itasca Consulting Canada Inc. A Mineral Reserve has been declared by AMEC and G Mining based on the National Instrument (“NI”) 43-101 compliant Mineral Resource authored by GeoStrat Consulting Inc. and published by Stornoway on January 24, 2011, and a diamond valuation conducted by WWW International Diamond Consultants Ltd. (“WWW”) and published by Stornoway on June 13, 2011. Highlights of the study are as follows:

-

Base case estimates of Net Present Value (“NPV”) of C$672 million at a 7% discount rate and Internal Rate of Return (“IRR”) of 18.7% before taxes and mining duties, and C$376 million and 14.9% after taxes and mining duties.

-

Probable Mineral Reserves of 18.0 million carats representing 23.0 million tonnes at an average grade of 78 carats per hundred tonnes (“cpht”), after allowance for mining dilution and ore recovery, and at a weighted average diamond valuation of US$180/carat.

-

11 year reserve-based mine life with maximum diamond production peaking at 2.1 million carats/annum, and averaging 1.7 million carats/annum life of mine.

-

Gross revenue, in real terms, of C$4,112 million and operating cash flow of C$2,677 million.

-

Initial estimated capital cost of C$802 million, including contingencies.

-

An estimated operating cost averaging C$54.71/tonne ($70.27/carat) life of mine, and yielding an operating margin of 68%.

Matt Manson, President and CEO, commented: “Today’s announcement is a significant milestone on the road towards Québec’s first diamond mine. This Feasibility Study presents a project with strong cash flow, a low risk operating profile, and robust margins. Our estimates for each capital, operating and revenue parameter are blue-chip and realistic. We foresee healthy project economics on the basis of the first 11 years of reserve-based mining alone. However, our Long Term Business Plan, which forms the basis of our mine permitting, allows for a significantly longer mine life based on the project’s total NI 43-101 Mineral Resources. Looking beyond the formal Mineral Resources, we have already identified a large quantity of exploration upside and each kimberlite is open at depth. As of today’s release, Renard is a diamond project with a positive Feasibility Study, a long and highly accretive resource tail, and clear-path permitting in one of the world’s best mining jurisdictions.”

Stornoway’s Board of Directors has approved the Renard FS for release and authorized proceeding to detailed engineering and project financing phases. A formal production decision is expected to be made following, among other things, the receipt of Certificates of Authorization from the relevant Québec and federal government regulatory authorities. In approving the release of the Renard FS, the Board of Directors noted the project’s key strengths as follows:

-

Positive base-case economics based on industry-standard assumptions for US dollar exchange rate, diamond pricing, fuel costing and discount rate.

-

Strong cash flow and an operating margin well positioned on the diamond industry cost curve.

-

Rigorous operating and capital cost estimation.

-

A detailed mine design validated by multiple levels of peer review.

-

Robust valuation sensitivities.

-

Well understood risks in each operating, geotechnical and environmental parameter, and an all season road for project construction and operation.

-

Pro-mining jurisdiction and strong social acceptance.

-

Highly accretive Long Term Business Plan based on an additional 17 million carats of Inferred Mineral Resources within the scope of the FS mine infrastructure but outside its economic scope in accordance with NI 43-101.

-

Extensive exploration upside at depth.

-

Grade and value upside through diamond breakage estimates and large diamond recovery forecasts not incorporated in the NI 43-101 Mineral Resource estimate or cash flow analysis.

-

Positive long term diamond market fundamentals.

Stornoway will host a conference call on the Renard FS on Wednesday, November 16, 2011 at 11am Eastern Standard Time. To participate in the call, dial 416-695-6616 or 800-766-6630 within North America, 00-800-4222-8835 within the UK, 001-800-4222-8835 within Hong Kong and + 800-4222-8835 internationally. A playback will be made available after the call by dialing 1-800-408-3053 (local access 905-694-9451) with the access code 4675200.

Additional support materials for the FS can be found on Stornoway’s website at http://stornowaydiamonds.com/renard/feasibility_study .

Feasibility Study

Mine Plan

The Renard FS outlines a combined open pit and underground mine based on a Mineral Reserve contained within the Renard 2, 3 and 4 kimberlite pipes. During years 1 and 2 production will be derived predominantly from an open pit at Renard 2 and 3 developed to a maximum depth of 113 meters and with a strip ratio of 5 to 1. Starting in year 2, production will be derived from an underground mine utilizing a 5.5 meter diameter shaft to 740 meters depth and access ramp. Underground mining of Renard 2 and 3 to a maximum depth of 610 meters will be by blast-hole shrink stoping with waste backfill placed from surface. Underground mining of Renard 4, which will commence in year 8, will be by blast-hole shrink stoping with waste backfill under a crown pillar. Nameplate ore processing capacity will be 6,000 tonnes per day (2.2 Mtonnes/annum) with maximum annual carat production exceeding 2 Mcarats/annum. Overall, 83% of diamond production will be from Renard 2, 8% from Renard 3 and 9% from Renard 4.

|

Table 1: Renard Feasibility Study Results and Key Assumptions |

|

|

Mining Parameters |

Reserve Carats (M) |

18.0 |

|

|

Tonnes Processed (M) |

23.0 |

|

|

Recovered Grade (cpht) |

78 |

|

|

Average Ore Recovery (%) |

83.5% |

|

|

Average Mining Dilution (%) |

13.5% |

|

|

Dilution Grade (cpht) |

0 |

|

|

Processing Rate (Mtonnes/annum) |

2.2 |

|

|

Mine Life (years) |

11 |

|

Cost Parameters |

Pre-Production Cap-ex (C$M) |

$802 |

|

|

LOM Cap-Ex (C$M) |

$994 |

|

|

Oil Price (US$/barrel) |

$90 |

|

|

LOM Op-ex (C$/tonne) |

$54.71 |

|

|

LOM Op-ex (C$/carat) |

$70.27 |

|

Revenue Parameters (real terms) |

Gross Revenue (C$M) |

$4,112 |

|

|

Marketing Costs |

2.7% |

|

|

DIAQUEM Royalty |

2.0% |

|

|

Cash Operating Margin (C$M) |

$2,677 |

|

|

% Operating Margin |

68% |

|

|

Total Taxes and Mining Duties (C$M) |

$571 |

|

|

After Tax Net Cash Flow (C$M) |

$1,151 |

|

Diamond Price Parameters |

Renard 2 and Renard 3 (US$/carat) |

$182 |

|

|

Renard 4 (US$/carat) |

$164 |

|

|

Diamond Price Escalation |

2.5% |

|

|

Exchange rate |

1C$=1US$ |

|

Schedule Parameters |

Effective Date for NPV Calculation |

January 1 2012 |

|

|

Construction Mobilization |

July 1 2013 |

|

|

Plant Commissioning Commences |

July 1 2015 |

|

|

Commercial Production Declared |

January 1 2016 |

|

Valuation Parameters |

Pre-Tax NPV7% (C$M) |

$672 |

|

|

Pre-Tax IRR |

18.7% |

|

|

After-Tax NPV7% (C$M) |

$376 |

|

|

After-Tax IRR |

14.9% |

|

|

|

Processed kimberlite management will be by way of a “dry-stack” disposal facility which may be progressively closed. Metal leach tests indicate that negligible metal concentrations will be released, thus no liner will be placed beneath the processed kimberlite containment facility. In addition, the operation of the processed kimberlite containment facility and waste disposal facilities will not impact fish habitats. The results of the Renard FS, and key assumptions used, are summarized in Table 1

The project development schedule assumes first vehicle access for construction mobilization by July 2013, based on the construction schedule for the Route 167 Extension project, a $332 million road development project sponsored by the Québec Ministry of Transportation under the auspices of the “Plan Nord” to which Stornoway has agreed to contribute an amount of C$44 million (subject to certain conditions). Plant production is currently anticipated to commence in July 2015 with a 2 month commission followed by a 6 month ramp-up period. On site power requirements are expected to average 10 MW during operations and be provided by on-site diesel power generation. A separate feasibility study authored by Hydro-Québec on a 161kV powerline connecting Renard to the nearby Laforge 1 hydro-electric powerstation is still ongoing. This powerline would add capital cost to the project but offers a substantial operating cost savings over diesel generated power. The powerline feasibility study is due to be completed later in 2012, and its impact on the Renard FS will be assessed at that time.

Long Term Business Plan

Stornoway has also developed a Long Term Business Plan (“LTBP”) based on the total Indicated and Inferred Mineral Resources to a depth of 700m, all of which are within the scope of the FS mine infrastructure. These include 6.1 Mcarats of high grade Inferred Mineral Resources between 600 and 700 meters depth in Renard 2. The LTBP also contemplates an increased production rate within the scope of the process plant’s design parameters, which allows for expansion up to 7,000 tonnes per day (2.6 Mtonnes/annum). Expansion mill feed is expected to be derived from an open pit on the Renard 65 kimberlite. Renard 65 is a large and lower grade deposit currently classified as Inferred Mineral Resource, but with diamond characteristics similar to the Renard 2 and 3 kimberlites. A pit at Renard 65 to a depth of 65 meters is included within the Renard FS as a borrow pit for backfill waste and for water management, and inferred mineralization recovered is stockpiled and excluded from the production schedule. Within the LTBP, the Renard 65 material will supplement higher grade ore from the Renard 2 and 3 underground mine. Although expected to be accretive to the Renard FS, the project’s Inferred Mineral Resources are not included in the FS economic analysis in accordance with NI 43-101. The LTBP is the basis of the Renard mine permit application, and as such will form part of the project’s public disclosure in connection with the environmental assessment regulatory process under applicable federal and provincial legislation.

Economic Analysis, Sensitivities and Diamond Price Assumptions

The Base Case financial model assumes a parity Canadian-US dollar exchange rate and diamond price models derived from an open market valuation exercise undertaken by WWW between May 9th-13th 2011. Diamond prices are escalated at 2.5% per annum in real terms between Q3 2011 and Q4 2025. Capital costs are escalated at between 1% and 4% per annum, item dependent. Operating costs, deferred capital and sustaining capital are escalated at 2% per annum. Net cash flows are then de-escalated for the calculation of rate of return and net present value on a real-terms basis (Table 2). Pre-tax NPV and IRR are calculated as of January 1st 2012 on net cash flow after operating costs, marketing costs and a 2% royalty payable to Diaquem Inc. After-tax NPV and IRR reflects the deduction of federal and Quebec income taxes and applicable mining duties. Pay-back is estimated, after-tax, at 4.8 years.

|

Table 2: Project Valuation and Pay-Back |

|

|

|

|

Pre-Tax |

After - Tax |

|

NPV5% |

$899 |

$534 |

|

NPV7% (Base Case) |

$672 |

$376 |

|

NPV9% |

$490 |

$248 |

|

IRR |

18.7% |

14.9% |

|

Pay-Back (years) |

4.65 |

4.80 |

Notes: Dollar amounts in C$ million.

Assuming an efficient execution of the project outlined in the Renard FS, the financial model shows a steep increase in NPV over the 4 year pre-production period between January 1st 2012 and the current target date of commercial production on January 1st 2016.

The project is most sensitive to estimated revenue parameters (diamond price, exchange rate and grade) and least sensitive to estimated operating cost metrics (Tables 3a and 3b). The project also shows strong sensitivity to future diamond price growth. Stornoway's utilization of a 2.5% real terms growth factor is consistent with well constrained rough diamond supply and demand forecasts and industry best-practice.

|

Table 3a: Sensitivity Analysis on Pre-Tax NPV7% |

|

|

|

|

|

-20% |

-10% |

0% |

+10% |

+20% |

|

Operating Cost |

$809 |

$740 |

$672 |

$603 |

$535 |

|

Capital Cost |

$830 |

$751 |

$672 |

$593 |

$514 |

|

Revenue1 |

$236 |

$454 |

$672 |

$890 |

$1,108 |

|

|

|

|

|

|

|

|

|

|

0% |

+2.5% |

+5% |

|

|

Diamond Price Escalation |

|

$227 |

$672 |

$1,228 |

|

|

|

|

|

|

|

|

|

Table 3b: Sensitivity Analysis on After-TaxNPV7% |

|

|

|

|

|

-20% |

-10% |

0% |

+10% |

+20% |

|

Operating Cost |

$464 |

$420 |

$376 |

$332 |

$287 |

|

Capital Cost |

$489 |

$432 |

$376 |

$319 |

$261 |

|

Revenue1 |

$95 |

$236 |

$376 |

$514 |

$651 |

|

|

|

|

|

|

|

|

|

|

0% |

+2.5% |

+5% |

|

|

Diamond Price Escalation |

|

$93 |

$376 |

$724 |

|

|

Notes: All figures in C$ million. |

|

|

|

|

|

1Includes Diamond Price, Exchange Rate and Grade |

|

|

|

|

The base case diamond price models determined by WWW in May 2011 were US$182/carat for Renard 2 and 3 and US$112/carat for Renard 4. The Feasibility Study base case diamond price models are derived from a value modeling approach that assumes a single diamond size distribution exists across the three kimberlites. This yields a higher diamond price model of US$164/carat for Renard 4. The alternative interpretation, that each kimberlite’s diamond population is unique and is correctly represented by its diamond sample, yields diamond price models of US$208/carat for Renard 2, US$165/carat for Renard 3 and US$112/carat for Renard 4. This “Alternative Diamond Price Model” is highly accretive to the project’s valuation given the dominance of Renard 2 in the mine plan. The interpretation of similarity in the diamond populations is the more conservative approach.

In establishing their diamond price models, WWW determined “High” and “Minimum” sensitivities on the base case diamond price based on alternate interpretations of diamond quality and size distribution. The WWW sensitivity limits are set such that, in the opinion of WWW, it is highly unlikely that an actual diamond price achieved for each kimberlite body upon production would fall below the “Minimum” sensitivity, but it is possible that the actual diamond price achieved may be higher than the “High” sensitivity, which is not a maximum price. Sensitivities on NPV7% and IRR have been generated for each of the WWW Minimum and High price scenarios, which are US$163 to US$236/carat for Renard 2, US$153 to US$205/carat for Renard 3 and US$105 to US$185/carat for Renard 4 (Tables 4a and 4b).

Table 4a: Diamond Price Sensitivities on Pre-Tax NPV7% |

|

|

|

Pre-Tax NPV7% |

IRR |

Pay-Back |

|

WWW Minimum Model |

$397 |

14.6% |

5.34 |

|

Base Case Model |

$672 |

18.7% |

4.65 |

|

Alternative Model |

$871 |

21.8% |

4.07 |

|

WWW High Model |

$1,261 |

26.5% |

3.49 |

|

|

|

|

|

Table 4b: Diamond Price Sensitivities on After-Tax NPV7% |

|

|

|

After-Tax NPV7% |

IRR |

Pay-Back |

|

WWW Minimum Model |

$199 |

11.5% |

5.46 |

|

Base Case Model |

$376 |

14.9% |

4.80 |

|

Alternative Model |

$502 |

17.4% |

4.20 |

|

WWW High Model |

$747 |

21.4% |

3.90 |

|

Notes: Dollar amounts in C$ million. |

|

|

Capital and Operating Costs

Initial capital costs are estimated at C$801.8 million, including a contingency of C$74.3 million. Capital cost is estimated at an accuracy of -13% and +17% (Table 5). Life of Mine capital cost, including escalation, sustaining and deferred capital, and provisions for pre-production revenue and salvage value, are estimated at C$994.4 million.

|

Table 5: Estimate of Capital Costs1 |

|

|

Site Preparation & General |

$ 22.9 |

|

Mining |

$ 236.9 |

|

Mineral processing plant |

$ 168.4 |

|

Onsite utilities and infrastructures |

$ 102.4 |

|

Owner's Cost |

$ 86.2 |

|

Spares, fills, tools |

$ 10.2 |

|

EPCM services |

$ 45.0 |

|

Field indirect costs, vendor representatives |

$ 22.5 |

|

Construction camp & Catering |

$ 25.0 |

|

Freight and duties |

$ 8.1 |

|

Contingency |

$ 74.3 |

|

Total Pre-Production Capital |

$ 801.8 |

|

Escalation Allowance on Initial Capital |

$ 57.3 |

|

Pre-Production Revenue |

$ (24.6) |

|

Deferred & Sustaining Capital3 |

$ 138.8 |

|

Deferred Capital (Route 167 Extension) |

$ 44.0 |

|

Salvage Value 2,3 |

$ (22.9) |

|

Total Life of Mine Capital, After Contingency, Escalation, Deferred and Sustaining Capital |

$ 994.4 |

|

Notes: All figures in C$ million. |

|

1 Totals may not add due to rounding. |

|

|

2 Calculated by Stornoway |

|

3 After Escalation |

Life of mine operating cost is estimated at C$54.71/tonne (C$70.27 per carat; Table 6) in Q2 2011 terms. The majority of open pit costs at Renard 2 and 3 occur before January 1st 2016 and are contained within the capital cost estimates. On a non-capitalized basis, open pit mining cost is estimated at C$19.99/tonne of ore in Q2 2011 terms.

|

Table 6: Estimate of Operating Costs1 |

|

|

|

|

C$ millions |

Unit Cost $/Tonne |

Unit Cost $/carat |

|

Open Pit Mine 2 |

$ 6 |

$ 0.27 |

$ 0.34 |

|

Underground Mine |

$ 556 |

$ 24.45 |

$ 31.41 |

|

Processing |

$ 344 |

$ 15.13 |

$ 19.43 |

|

G&A |

$ 338 |

$ 14.86 |

$ 19.09 |

|

Total Life of Mine Operating Costs |

$ 1,244 |

$ 54.71 |

$ 70.27 |

|

Notes: All figures in Q2 2011 C$. |

|

|

|

1 Totals may not add due to rounding. |

|

2 Not including pit costs capitalized prior to January 1st, 2016. |

Mineral Reserves and Mineral Resources

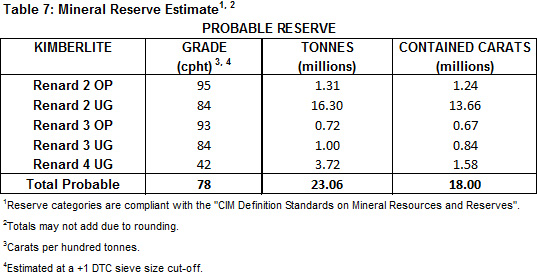

The Mineral Reserve estimate, prepared by AMEC and G Mining (Table 7), was derived from the NI 43-101 compliant Indicated Mineral Resource estimate announced by Stornoway on January 24th 2011 and dated February 3rd 2011. The Mineral Reserve estimate incorporates estimates for internal dilution (representing the quantity of non-resource material contained within the pit and stope design), mining recovery within the pits and stopes, and external dilution from adjacent country rock. Mining recovery estimates are 96% in the open pits and 82.4% in the underground mine. External dilution estimates are 7-11% in the open pits and 14% in the underground mine. Assumed dilution grade is 0 cpht.

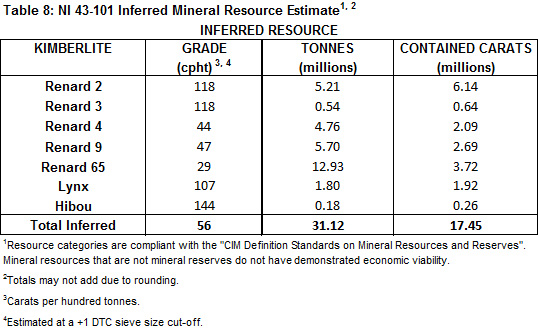

The NI 43-101 compliant Inferred Mineral Resources comprise an additional 17.5 Mcarats representing 31.1 Mtonnes at an average grade of 56 cpht (Table 8). In addition to these mineral resources, GeoStrat estimated the quantity of an exploration target (previously referred to by Stornoway as a “Potential Mineral Deposit”) to be 23.5 to 48.5 Mcarats (55.1 to 75.5 Mtonnes at grades ranging from 23 to 188 cpht). This exploration target within the Renard kimberlite pipes has been determined by projecting kimberlite volumes from the base of the Inferred Resource to a depth of approximately 775m below surface, representing the base of current drilling as established at Renard 4. Readers are cautioned that the potential quantity and grade of any such exploration target is conceptual in nature, there has been insufficient exploration to define a mineral resource, and it is uncertain if further exploration will result in the target being delineated as a mineral resource. Readers are referred to the NI 43-101 compliant technical report dated February 3rd 2011 filed by Stornoway on SEDAR at www.sedar.com with respect to the disclosure of Mineral Resources for the Renard Diamond Project.

Permitting

The Renard Diamond Project falls under the environmental protection regimes of the James Bay and Northern Québec Agreement (the “JBNQA”) and the Canadian Environmental Assessment Act. Stornoway expects to file the project’s Environmental and Social Impact Assessment shortly and, subject to a schedule to be established by the Review Committee of the JBNQA (“COMEX”) and the Canadian Environmental Assessment Agency, it is currently expected that public hearings will be held in the first half of 2012. Upon the satisfaction of all regulatory requirements, it is currently anticipated that the project will be eligible for the receipt of both Québec and Federal Certificates of Authorization by the middle of 2012. Once the provincial and federal administrators have issued authorizations for project development, final mine permits will be sought from the Québec Ministère du Développement durable, de l'Environnement et des Parcs, the Ministère des Ressources Naturelles et de la Faune, and all relevant federal authorities.

Community Relations

In collaboration with the Crees of the James Bay region, Stornoway undertakes regular consultations with local communities, including public open houses and individual stakeholder meetings. Since the beginning of this year the Renard Environmental Exchange Group has met in the Cree community of Mistissini six times, giving a forum for the exchange of environmental and traditional knowledge, and interaction in the project design. Stornoway also is currently in negotiations with Mistissini and the Grand Council of the Crees (Eeyou Istchee) with the aim of concluding an Impact and Benefits Agreement. This agreement is expected to provide mine related employment and contracting opportunities, as well as foster environmental and social protection. This negotiation process follows the successful execution of a Pre-Development Agreement between the parties in July 2010, and the establishment of a project business development office in the community of Mistissini in January of this year. The financial impact of the Impact and Benefits Agreement has not been incorporated into the FS or the revenues and cost estimates presented in this press release.

Qualified Persons

Mr. Ab Kroon, P.Eng. of SNC Lavalin Inc. is the independent Qualified Person responsible for infrastructure design, the operating and capital cost estimate, and risk management.

Dr. Lynton Gormely, P.Eng. of AMEC Americas Limited is the independent Qualified Person responsible for process plant design.

Mr. Gary Taylor, P.Eng. of AMEC Americas Limited is the independent Qualified Person responsible for underground mine design and mineral reserves.

Mr. Louis-Pierre Gignac, Eng. of G Mining Services Inc. is the independent Qualified Person responsible for open pit design and mineral reserves, and financial analysis.

Mr. Martin Magnan, Eng. of Roche Lte. is the independent Qualified Person responsible for permitting and environmental and social considerations.

Mr. Paul Bedell, P.Eng. of Golder Associates Ltd. is the independent Qualified Person responsible for geotechnical, water management and processed kimberlite containment facility design.

Ms. Valérie Bertrand, Géo. of Golder Associates Ltd. is the independent Qualified Person responsible for geochemical classification.

Mr. Richard Brummer, P.Eng. of Itasca Consulting Canada Inc. is the independent Qualified Person responsible for geomechanical and hydrogeological considerations.

Mr. David Farrow, P.Geo. (BC) of GeoStrat Consulting Inc. is the independent Qualified Person responsible for the preparation of the mineral resource estimate for the Renard Diamond Project.

Stornoway's diamond exploration programs are conducted under the direction of Robin Hopkins, P.Geo. (NT/NU), Vice President, Exploration, a Qualified Person under NI 43-101.

All of these Qualified Persons have reviewed and approved the contents of this press release for which they are responsible.

Stornoway will file a NI 43-101 compliant technical report on the Renard FS within 45 days.

About Stornoway Diamond Corporation

Stornoway is a leading Canadian diamond exploration and development company listed on the Toronto Stock Exchange under the symbol SWY. Our flagship asset is the 100% owned Renard Diamond Project, on track to becoming Québec's first diamond mine. Stornoway also maintains an active diamond exploration program with both advanced and grassroots programs in the most prospective regions of Canada. Stornoway is a growth oriented company with a world class asset, in one of the world's best mining jurisdictions, in one of the world's great mining businesses.

On behalf of the Board

STORNOWAY DIAMOND CORPORATION

/s/ "Matt Manson"

Matt Manson

President and Chief Executive Officer

For more information, please contact Matt Manson (President and CEO) at 416-304-1026

or Nick Thomas (Manager Investor Relations) at 604-983-7754, toll free at 1-877-331-2232

Pour plus d'information, veuillez contacter M. Ghislain Poirier, Vice-président Affaires publiques de Stornoway au 418-780-3938, gpoirier@stornowaydiamonds.com

** Website: www.stornowaydiamonds.com Email: info@stornowaydiamonds.com **

This press release contains "forward-looking information" within the meaning of Canadian securities legislation and "forward-looking statements" within the meaning of the United States Private Securities Litigation Reform Act of 1995. This information and these statements, referred to herein as "forward-looking statements", are made as of the date of this press release and the Company does not intend, and does not assume any obligation, to update these forward-looking statements, except as required by law.

Forward-looking statements relate to future events or future performance and reflect current expectations or beliefs regarding future events and include, but are not limited to, statements with respect to: (i) the amount of mineral resources and exploration targets; (ii) the amount of future production over any period; (iii) net present value and internal rates of return of the mining operation; (iv) assumptions relating to capital costs, operating costs and other cost metrics set out in the Feasibility Study; (v) assumptions relating to gross revenues, operating cash flow and other revenue metrics set out in the Feasibility Study; (vi) assumptions relating to recovered grade, average ore recovery and other mining parameters set out in the Feasibility Study; (vii) mine expansion potential and expected mine life; (viii) expected time frames for completion of permitting and regulatory approvals and making a production decision; (ix) future exploration plans; (x) future market prices for rough diamonds; and (xi) sources of and anticipated financing requirements. Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, assumptions or future events or performance (often, but not always, using words or phrases such as "expects", "anticipates", "plans", "projects", "estimates", "assumes", "intends", "strategy", "goals", "objectives" or variations thereof or stating that certain actions, events or results "may", "could", "would", "might" or "will" be taken, occur or be achieved, or the negative of any of these terms and similar expressions) are not statements of historical fact and may be forward-looking statements.

Forward-looking statements are made based upon certain assumptions by Stornoway or its consultants and other important factors that, if untrue, could cause the actual results, performances or achievements of Stornoway to be materially different from future results, performances or achievements expressed or implied by such statements. Such statements and information are based on numerous assumptions regarding present and future business strategies and the environment in which Stornoway will operate in the future, including the price of diamonds, anticipated costs and ability to achieve goals. Certain important factors that could cause actual results, performances or achievements to differ materially from those in the forward-looking statements include, but are not limited to: (i) estimated completion date for the Environmental and Social Impact Assessment; (ii) required capital investment and estimated workforce requirements; (iii) estimates of net present value and internal rates of return; (iv) receipt of regulatory approvals on acceptable terms within commonly experienced time frames; (v) the assumption that a production decision will be made, and that decision will be positive; (vi) anticipated timelines for the commencement of mine production; (vii) anticipated timelines related to the Route 167 extension and the impact on the development schedule at Renard; (viii) anticipated timelines for community consultations and the conclusion of an Impact and Benefits Agreement; (ix) market prices for rough diamonds and the potential impact on the Renard Project's value; and (x) future exploration plans and objectives.

By their very nature, forward-looking statements involve inherent risks and uncertainties, both general and specific, and risks exist that estimates, forecasts, projections and other forward-looking statements will not be achieved or that assumptions do not reflect future experience. We caution readers not to place undue reliance on these forward-looking statements as a number of important risk factors could cause the actual outcomes to differ materially from the beliefs, plans, objectives, expectations, anticipations, estimates, assumptions and intentions expressed in such forward-looking statements. These risk factors may be generally stated as the risk that the assumptions and estimates expressed above do not occur, including the assumption in many forward-looking statements that other forward-looking statements will be correct, but specifically include, without limitation, (i) risks relating to variations in the grade, kimberlite lithologies and country rock content within the material identified as mineral resources from that predicted; (ii) variations in rates of recovery and breakage; (iii) the greater uncertainty of exploration targets; (iv) developments in world diamond markets; (v) slower increases in diamond valuations than assumed; (vi) risks relating to fluctuations in the Canadian dollar and other currencies relative to the US dollar; (vii) increases in the costs of proposed capital and operating expenditures; (viii) increases in financing costs or adverse changes to the terms of available financing if any; (ix) tax rates or royalties being greater than assumed; (x) results of exploration in areas of potential expansion of resources; (xi) changes in development or mining plans due to changes in other factors or exploration results of Stornoway; (xii) changes in project parameters as plans continue to be refined; (xiii) risks relating to receipt of regulatory approvals or the conclusion of an Impact and Benefits Agreement with aboriginal communities; (xiv) the effects of competition in the markets in which Stornoway operates; (xv) operational and infrastructure risks; and (xvi) the additional risks described in Stornoway's most recently filed Annual Information Form, annual and interim MD&A, and Stornoway's anticipation of and success in managing the foregoing risks. Stornoway cautions that the foregoing list of factors that may affect future results is not exhaustive.

When relying on our forward-looking statements to make decisions with respect to Stornoway, investors and others should carefully consider the foregoing factors and other uncertainties and potential events. Stornoway does not undertake to update any forward-looking statement, whether written or oral, that may be made from time to time by Stornoway or on our behalf, except as required by law.